Provided all advantages listed above, a seasoned that have a Va mortgage could possibly get question why he or she may want to refinance on a traditional financing. Whatsoever, new Va mortgage generally seems to give substantially.

Reasons why you should Re-finance an effective Va Financing

- Convert Dated Household towards the a rental Possessions

- Re-finance so you can a traditional Loan which have Best Conditions

- To make use of an enthusiastic IRRRL

Transfer Dated Home for the accommodations Assets

Usually, you simply cannot play with an effective Virtual assistant mortgage buying the next property if for example the first assets (your primary residence) happens to be financed with its very own Va financing. not, a common behavior is for the fresh new experienced to re-finance their present Virtual assistant mortgage (on their primary home) for the a traditional financing.

Following, they can fool around with one minute Virtual assistant loan to purchase the next possessions which he normally move into to make their new number one household. Their old home may then end up being turned into accommodations possessions of which he is able to earn additional money.

Refinance so you’re able to a normal Mortgage which have Most readily useful Conditions

One other reason so you can refinance an excellent Virtual assistant mortgage toward a normal loan is to try to introduce better conditions towards the mortgage. Essentially, an experienced wouldn’t do that except if she had been staying in their own house getting an adequate long time.

Therefore, because the rates of interest change over the years, something special-go out conventional mortgage you will promote finest terminology than simply their original Va mortgage which had been funded unnecessary years back. Along with, consider the fact that she’ll features accumulated equity for the their own home. When it security exceeds 20%, the reality that Virtual assistant loans not one of them a down-payment or PMI gets irrelevant.

Furthermore, if a veteran features a high sufficient credit score, he may be capable of getting a normal that just offers most useful words than simply their newest Va loan.

To utilize an IRRRL

An enthusiastic IRRRL (Rate of interest Avoidance Refinance mortgage) try a new program supplied by this new Va getting experts exactly who want to refinance a good Va financing. They provides so you can streamline the entire process of refinancing in order to allow experienced to go with the a loan having a lesser rate of interest.

Although not, if a veteran possess numerous mortgage loans, she will most likely not be eligible for this method. Thus, she may decide to refinance on the a normal financing, if this sounds like the only path she will be able to progress pricing.

Now that we now have discussed as to why a seasoned would like to re-finance an payday loans Kingston effective Va financing to help you a normal loan, why don’t we talk about how this is done.

How can you Refinance a good Va Loan to a traditional?

If the a veteran determines the guy would like to re-finance an excellent Virtual assistant loan to help you a normal financing, the guy is to begin by organizing his pointers right after which after the a step-by-action technique to get the task over. There are certain issues that must be looked after out-of also various other elective details which will feel looked at.

Glance at Your financial Wellness

The very first thing a seasoned will have to score a feeling from was his full monetary fitness. This article is important for the latest borrower provide your an excellent sense of in which the guy really stands and you may exactly what they can do heading send. Most of the time, the majority of this information is as well as necessary for the financial institution. Whatsoever, the lender have a great vested interest in since brand new borrower can be well-off financially as you are able to.

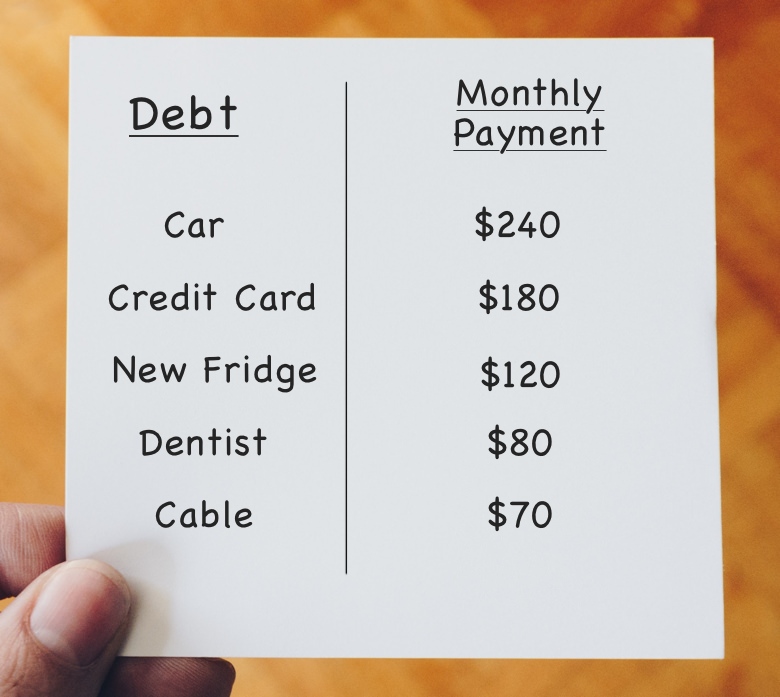

- Equity: Regardless of if verifying the guarantee isn’t compulsory, it is sensible. Also, regardless if with 20 percent collateral of your home actually an outright needs, it can save you from buying PMI. Should you choose fall short from 20 percent as well as have to help you shell out PMI, you will need to component that to your month-to-month budget.